Beneficiary Planner Guide: Secure Your Legacy in 2025

You’re going to die. Sorry, but someone had to say it. The real question is, will you leave your family a smooth ride or a legal circus that would make reality TV jealous?

A beneficiary planner is not just some boring paperwork, it’s your ticket to making sure your legacy lands where you want, not in your ex’s lap or Uncle Sam’s greedy paws.

In this guide, we’ll break down why you need a beneficiary planner, walk you through each step, highlight legal must-knows, expose common traps, and serve up the best tools for a peaceful afterlife (for everyone else, at least).

Start planning your death party now and save your family from chaos.

Why Beneficiary Planning Matters in 2025

Picture this: You’re gone, and your family’s new favorite hobby is fighting over your stuff. Not exactly the legacy you want, right? That’s where a beneficiary planner steps in, like a referee for your death party. In 2025, ignoring this tool is basically inviting chaos to your family’s doorstep.

The Rising Stakes of Estate Planning

Let’s talk money, drama, and the law. Dying without a beneficiary planner these days is like throwing your family into a legal game show, except the prize is a $29,500 bill for probate fees. That’s not even counting what your cousin will spend on therapy after fighting with your ex over your PlayStation.

America is aging, and more assets are changing hands than ever. The government noticed, too. In 2025, estate tax thresholds are shifting, and digital assets like your crypto and that embarrassing TikTok account are now considered fair game. If you don’t spell out who gets what, expect family feuds worthy of reality TV.

And don’t forget: unclear wishes mean more than just legal headaches. They rip families apart. Siblings stop speaking, spouses lawyer up, and nobody remembers you for your killer lasagna recipe—just the mess you left behind.

Quick Glance: What’s at Stake?

| Risk | Cost/Impact |

|---|---|

| Probate fees | $29,500+ |

| Family disputes | Broken relationships, lawsuits |

| Legal confusion | Delays, extra expenses |

| Unclaimed assets | Lost to the state |

Real-World Consequences: What Happens Without a Beneficiary Planner

Think this is just scare talk? According to the 2025 Trust & Will Estate Planning Report, a whopping 55% of Americans have zero estate documents. That’s over half the country rolling the dice with their family’s future. The result? Grieving families tangled in red tape, assets frozen, and siblings fighting over grandma’s hideous lamp.

Here’s a real gem: One family spent months in court because dad never updated his beneficiary planner after remarrying. The ex-wife took the house, the new wife got the bills, and the kids got a crash course in why procrastination is expensive.

The emotional toll is brutal. Instead of mourning, your loved ones are stuck deciphering bank statements and arguing with lawyers. Thanks, Dad.

Security for Your Legacy: How a Beneficiary Planner Prevents Chaos

So, what’s the alternative? A beneficiary planner is your posthumous mic drop. It spells out who gets what, keeps the government’s grubby hands off your assets, and lets your family grieve without extra drama. Want to make sure your ex doesn’t get your PlayStation? Write it down.

Having a beneficiary planner means your wishes are followed, your legacy is protected, and your family actually remembers you fondly. You get peace of mind, and they get clarity instead of chaos. It’s the least you can do for the people who have to clean out your sock drawer.

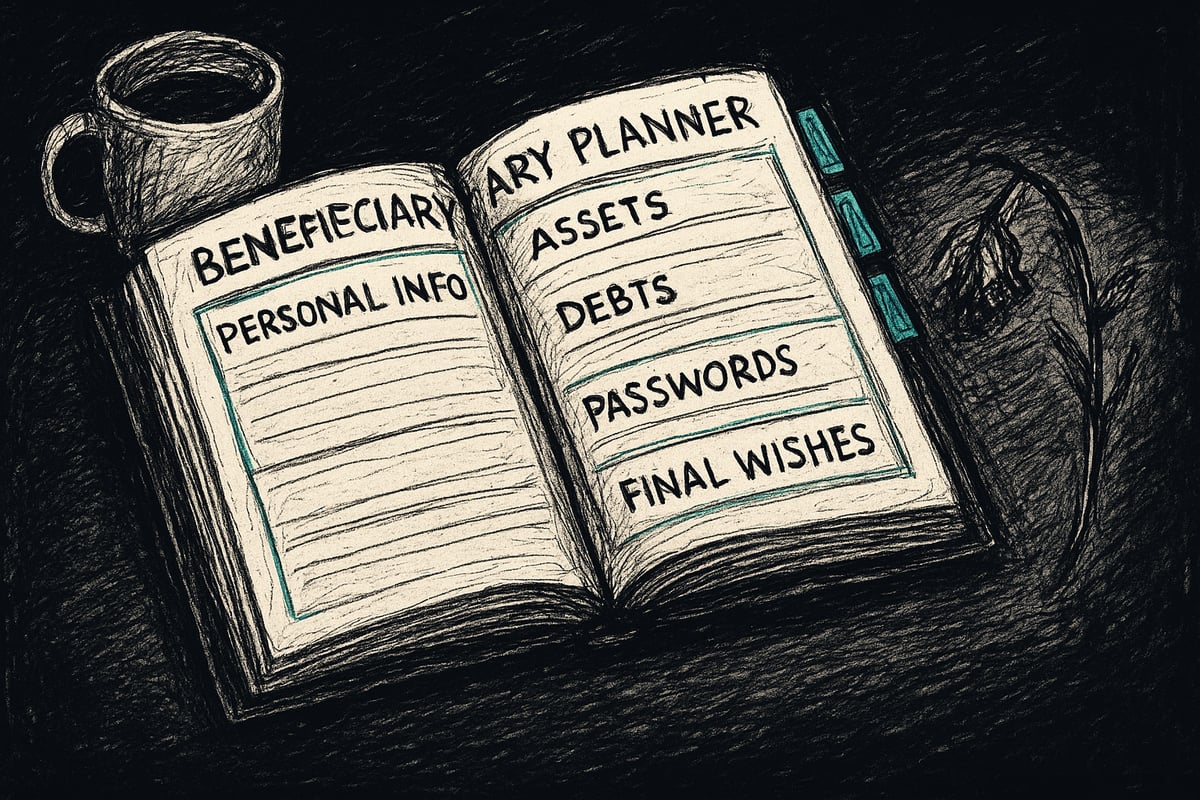

Core Components of a Beneficiary Planner

So, you’ve finally accepted your mortality and decided to get your act together. Welcome to the party. But before you pat yourself on the back, let’s get real: a beneficiary planner isn’t just a glorified to-do list scribbled on a napkin. It’s your shield against chaos, confusion, and that one cousin who thinks they’re entitled to your vintage record collection.

What Every Beneficiary Planner Should Include

First things first: your beneficiary planner needs more than your name and a wish for “no drama.” Here’s what separates the responsible from the reckless:

- Personal Information: Not just your name, but dates of birth, contact info, and Social Security numbers. If you want your heirs to find you—or what’s left of you—make it easy.

- Asset Inventory: List every asset you own. House, bank accounts, 401(k), crypto, the secret Beanie Baby stash. Assign values and account numbers. Digital assets? Yes, those embarrassing Twitter drafts count.

- Debts and Liabilities: Mortgages, credit cards, that loan you took for a hot tub in 2009. List it all. Your family shouldn’t discover surprise debts while grieving.

- Beneficiary Designations: Spell out who gets what. Don’t forget alternates in case your primary beneficiary has the nerve to die first.

- Funeral and Final Wishes: Your playlist for the “death party,” burial or cremation, and who’s writing your legendary obituary.

- Legal Documents: Where’s your will? Power of attorney? Healthcare directives? If it’s “somewhere safe,” be specific.

- Access Instructions: Passwords, safe deposit boxes, secret handshakes—leave instructions that won’t require a séance.

Want the full checklist? Check out Kiplinger’s Guide to Estate Planning Basics for a rundown of what you can’t afford to miss in your beneficiary planner.

Here’s a handy table to roast your planning skills:

| Component | Comprehensive Planner | Incomplete Planner |

|---|---|---|

| Personal Info | Full details | Only names |

| Asset Inventory | All assets listed | “I think I had a 401k?” |

| Debts/Liabilities | All debts specified | “Surprise! More bills!” |

| Beneficiary Designations | Clear, with backups | Vague or missing |

| Legal Docs Location | Exact places noted | “In a drawer…maybe?” |

| Access Instructions | Passwords included | “Good luck hacking in” |

Example: Comprehensive vs. Incomplete Planners

Picture this: Two families, both mourning, but only one is also cursing your name. The first family finds a beneficiary planner with everything—personal info, assets, who gets the dog, and even your WiFi password. They settle your affairs, have a toast, and move on (mostly).

The second family? They find sticky notes, cryptic hints, and a “will” written in crayon. No clear beneficiary planner, no idea who gets what, and suddenly, everyone’s lawyered up. Your prized guitar? Now Exhibit A in a courtroom drama.

A strong beneficiary planner is your last act of responsibility. By making yours thorough, you save your loved ones from legal limbo and family feuds. Don’t half-bake your legacy. Make sure you cover all the bases, from assets to access instructions. Death is free, but a messy estate plan costs a fortune.

Step-by-Step: How to Create a Beneficiary Planner in 2025

You know what’s fun? Not leaving your family a hot mess when you’re gone. Creating a beneficiary planner is like throwing a party for your future ghost—except you’re the only one who knows where the snacks are hidden. Let’s break this down so you can stop procrastinating and start being the responsible adult you pretend to be at work.

1. Gather and Organize Your Information

First, let’s channel your inner detective. Dig up everything: real estate deeds, bank account numbers, investment statements, even that dusty crypto wallet you forgot existed. Don’t forget debts, because yes, your student loans are still haunting you.

Make a checklist—here’s your cheat sheet:

- Assets: Homes, cars, accounts, digital junk

- Liabilities: Mortgages, loans, credit cards

- Beneficiaries: Full names, birthdates, why you like them (or don’t)

- Legal docs: Will, trust, power of attorney, healthcare directives

A beneficiary planner that’s missing key info is like a treasure map with half the landmarks erased. Spoiler: No one finds the loot.

2. Choose the Right Tools and Templates

Paper planners are great if you like the thrill of losing things. Digital organizers, though, let you update from your couch during a Netflix binge. Features to hunt for: big print, clear sections, and maybe a joke or two so you don’t cry.

Want to go full 2025? Consider a cross-platform digital solution like Beyond Life: A Digital Will Solution. It lets you manage your beneficiary planner online, so your heirs can’t claim they “lost the binder.”

Compare options:

| Tool Type | Pros | Cons |

|---|---|---|

| Paper | Tangible, simple | Prone to loss, hard to update |

| Digital | Secure, editable, shareable | Needs password, tech-savvy |

3. Document Your Wishes Clearly

Write your wishes like you’re explaining them to a goldfish—no legalese, just plain talk. Spell out who gets what, and don’t leave your intentions up for a family debate worthy of reality TV.

Include:

- Specific distributions (“Aunt Linda gets the cat, not the house”)

- Contingency plans (what if someone predeceases you)

- Personal notes (because you’re sentimental, not heartless)

A beneficiary planner filled with vague instructions is an open invitation for drama. Save the plot twists for your memoir.

4. Store and Share Securely

Don’t just toss your beneficiary planner in a sock drawer. Store it in a home safe, a digital vault, or with your attorney—somewhere your heirs will actually look. Decide who gets access: your executor, trusted family, maybe not your freeloading cousin.

Set reminders to update as life changes. Outdated info is a legal time bomb. Share access securely, and make sure your chosen few know where to find your plan when the time comes.

Congrats! You’re now slightly less irresponsible than you were 10 minutes ago.

Legal Considerations and Avoiding Common Pitfalls

Navigating the legal labyrinth of estate planning in 2025 is about as fun as a root canal, but hey, at least the root canal only hurts your mouth. Your beneficiary planner, if done wrong, can hurt your entire family. State laws are like snowflakes: no two are the same, and they can all melt your best-laid plans if you ignore them.

If your will isn’t legally airtight, congrats, you just bought your heirs a ticket to Probate Purgatory. Spoiler: it’s expensive, slow, and makes family drama look like a soap opera rerun. Naming your beneficiaries with the precision of a surgeon is non-negotiable. “My kids” isn’t going to cut it when your ex’s lawyer comes knocking.

Let’s get real—life happens. Marriages, divorces, new babies, old grudges. Only 40% of Americans bother to update their plans after major life changes, which means the rest are playing legal roulette with their legacy. Don’t be that person who leaves their crypto wallet to the dog because you forgot to update your beneficiary planner after adopting Mr. Fluffy.

Here’s a look at some classic estate planning fails:

| Pitfall | Disaster Outcome |

|---|---|

| Outdated beneficiary planner | Ex gets your PlayStation |

| No digital assets listed | Bitcoin lost in cyberspace |

| Vague beneficiary language | Family feud on Judge Judy |

| Missing will or POA | Court decides everything |

Oh, and 2025 is changing the rules again: estate tax exemptions, digital asset laws, you name it. For the gory details, check out KPMG’s Estate Planning in 2025 Report and try not to lose sleep.

Killswitch: The Modern Estate Planning Solution

Traditional legal services for your beneficiary planner are about as user-friendly as a tax audit. You pay thousands, get buried in paperwork, and wait months for an answer. By the time you’re done, you’ve aged a decade and your family is still not protected.

Killswitch is the estate-planning equivalent of ripping off a Band-Aid—quick, effective, and way less painful than the alternatives. For a one-time $69 fee, you get a legally valid will in all 50 states, unlimited updates, and instant download. That means you can tweak your beneficiary planner every time your life takes a sharp left turn—no extra charges, no fine print, just the sweet sound of peace of mind.

No legal jargon. No hidden fees. No waiting for some suit to call you back. Just bank-level security, a process that takes less than 30 minutes, and a guarantee your family won’t have to arm-wrestle in court over your collection of rare Beanie Babies.

If you want your legacy to be more “well-loved parent” and less “cautionary tale on Reddit,” do yourself a favor: get your beneficiary planner in order and make it idiot-proof.

Beneficiary Planner Templates, Tools, and Resources for 2025

Congratulations, you’ve finally accepted that you’re mortal. Now, let’s make sure your beneficiary planner is something your future ghost won’t be embarrassed by. The world of planners is a jungle, but don’t worry, you don’t need a machete—just a sense of humor and a willingness to admit you have stuff people might actually want.

Guided Estate Planning Organizers: Because You Need a Checklist for Your Checklist

Let’s face it, you’d lose your head if it wasn’t attached. That’s why a guided estate planning organizer is your new best friend. A good beneficiary planner comes with step-by-step checklists so you don’t forget your crypto wallet, your grandmother’s cursed ring, or that secret bank account you swore you’d close.

Look for planners that break down the process into manageable bites. Some even include prompts for those “oh right, I own a timeshare in Florida” moments. A beneficiary planner that provides clear sections for assets, debts, and final wishes saves your family from playing detective after you’re gone.

Two words: structure and sanity. If your planner makes you laugh or at least doesn’t bore you to death, you’re on the right track.

Digital vs. Physical Planners: Paper Cuts or Passwords?

Do you want your beneficiary planner on paper, or would you rather trust your legacy to the cloud? Let’s compare, because this is a battle as old as, well, the internet:

| Feature | Digital Planners | Physical Planners |

|---|---|---|

| Accessibility | Anywhere, anytime | Wherever you left it |

| Updates | Instant, unlimited | White-out required |

| Security | Encryption, passwords | Fireproof safes |

| User Experience | Searchable, clickable | Tangible, tactile |

If you’re the type who forgets passwords, maybe go old-school. If you lose everything that isn’t glued to your phone, digital might be your jam. Either way, your beneficiary planner should be easy to access for the right people and impossible for your nosy ex.

Features, Prices, and Where to Find the Good Stuff

A truly helpful beneficiary planner isn’t just a glorified notebook. Prioritize these features:

- Humor and plain language

- Large, readable text (because squinting is for the young)

- Ample writing space for your “special” instructions

Prices range wildly, from $7.99 for a basic downloadable template to $20+ for spiral-bound, senior-friendly organizers. Want the digital vault experience? Expect to pay a little more, but hey, your secrets are safe.

User reviews reveal the truth: the best planners are easy to follow and don’t require a law degree. For templates and legal guidance, check reputable estate planning sites like Nolo. Your family will thank you—and so will your conscience.

Keeping Your Beneficiary Planner Up to Date

Congratulations, you’ve finally started your beneficiary planner. Now, here’s the bad news: life doesn’t care about your paperwork. It changes, constantly. If you think your first draft is your last, you’re basically inviting your ex to crash your death party and claim your stuff.

Update Triggers: The “Congratulations, You Now Need to Fix Your Plan” List

Let’s be real: every major life event is a reason to revisit your beneficiary planner. Did you get married, divorced, or have a baby? Did your favorite nephew suddenly become your least favorite? Maybe you bought a house, or your dog inherited a trust fund. All these are triggers.

Common Triggers Table

| Event | Update Needed? |

|---|---|

| Marriage | Yes |

| Divorce | Yes |

| Birth/Adoption | Yes |

| Death in Family | Yes |

| New Asset | Yes |

| Major Move | Yes |

If you’re waiting for a sign, this is it. Your beneficiary planner is not a crockpot. You can’t just set it and forget it.

Annual Reviews: The Guilt Trip You Need

Set a calendar reminder for your annual “Am I Still Alive and Responsible?” check-in. Once a year, dust off your beneficiary planner, pour a drink, and make sure your ex isn’t still listed as your life insurance beneficiary.

Regular reviews save your loved ones from expensive legal drama. There’s nothing like a $20,000 probate bill to haunt your family because you couldn’t spend 10 minutes updating a name.

Communicate with Your Beneficiaries (Yes, That Means Talking to Them)

Transparency is awkward but necessary. Tell your beneficiaries about your plans. Don’t let them find out after you’re gone that your crypto wallet password is “password123.” Avoiding this conversation is like hiding a ticking time bomb in your estate.

Secure Sharing: Grant Access, Not Chaos

Keep your beneficiary planner somewhere safe, but don’t lock it up like the crown jewels. Share access with your executor, a trusted family member, or your attorney. Use digital planners that let you update and share securely, so you’re not relying on your memory (or your dog’s).

Outdated Info: The Ghost of Legal Battles Yet to Come

You know what’s scarier than dying? Outdated information. If you forget to update your beneficiary planner, your family could be stuck in court, fighting over your collection of questionable NFTs. Regular updates prevent this horror story.

Tools and Traditions: Make Updating Painless

Embrace digital tools that allow unlimited edits. Set reminders on your phone or mark your calendar every year. Make updating your beneficiary planner a family tradition, like awkward Thanksgiving dinners, but more useful.

Congrats! You’re now slightly less irresponsible than you were ten minutes ago. Keeping your beneficiary planner alive keeps your legacy (and your family) out of chaos.

Look, you made it this far—which already puts you ahead of 67 percent of adults still dodging the whole “what happens when I die” conversation. Here’s the blunt truth: you’re not immortal, your family is probably not psychic, and if you don’t get your wishes down, chaos is basically guaranteed. Why let a judge (or worse, your ex) decide where your stuff goes? It takes less time than arguing with your siblings and costs less than a fancy dinner. Ready to finally be a responsible grown up and save your loved ones a legal migraine? Start My Will Now